5 Key Areas to Watch to Keep Your Benefit Plan in Compliance

Employers who offer employee benefit plans like health insurance or retirement benefits are governed by the Employee Retirement Income Security Act...

1 min read

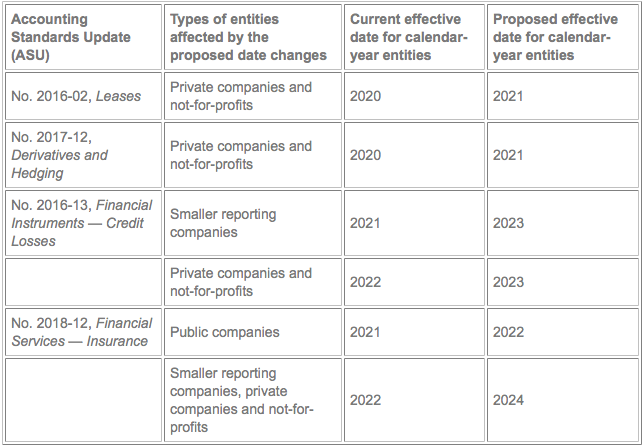

On July 17, the Financial Accounting Standards Board (FASB) voted to issue a proposal that would delay several landmark accounting rules for certain companies. If finalized, the deferral would apply to new guidance for reporting leases, hedging transactions, credit losses and long-term insurance contracts.

Summary of the changes

The following table summarizes key implementation date changes that the FASB unanimously voted to propose:

The term “smaller reporting companies” refers to those that have either 1) a public float of less than $250 million, or 2) annual revenue of less than $100 million and no public float or a public float of less than $700 million.

Unexpected delays

Private companies and nonprofits often receive an extra year to implement major accounting standards updates, compared to the effective dates that apply to public companies. In a shift in its philosophy for setting reporting dates on major new accounting standards, the FASB wants to give certain entities even longer to implement the changes.

Why are these delays needed? Many entities continue to struggle with implementing the new revenue recognition guidance that went into effect in 2018 for public companies and 2019 for other entities. A possible deferral of other new rules would also allow smaller entities to learn from public companies how to implement the changes — and it would give accounting software providers extra time to update their packages to support the new reporting models.

Proposal is coming soon

The FASB is expected to issue its proposal as soon as possible. Then it will be subject to a 30-day comment period.

These deferrals, if finalized, would be welcome news for many organizations. But they’re not an excuse to procrastinate. Depending on your industry and the nature of your transactions, implementing the changes and educating stakeholders could take significant resources. Contact us before the implementation deadline to come up with a realistic game plan.

© 2019

Employers who offer employee benefit plans like health insurance or retirement benefits are governed by the Employee Retirement Income Security Act...

QuickBooks Online is an important piece of software because it helps ensure the accuracy of your financial records with a little help from your bank...

Under federal law, most organizations with an employee benefit plan that has 100 or more participants with account balances at the beginning of the...